Alternatives to Reverse Mortgages in Canada — A Plain-English Comparison

A reverse mortgage isn't right for everyone. This page is for the people who want to understand every option before deciding.

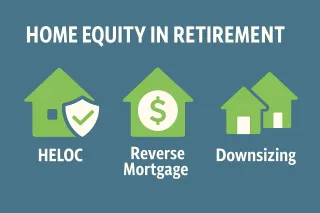

A reverse mortgage is not the only way to access home equity in retirement. It is not always the right way. This page covers every meaningful alternative — what each one offers, what it requires, what it actually costs, and when it makes more sense than a reverse mortgage.

The goal isn't to steer you toward or away from a reverse mortgage. It's to make sure the comparison is real — including the comparison most people never make, which is what downsizing actually costs in a major Canadian market once you run the full transaction numbers.

On this page: Summary Table · HELOC · Conventional Refinance · Second Mortgage · Downsizing · Rental Income · Registered Account Draws · No-Payment Term Mortgage · Property Tax Deferral · How to Choose · FAQ · Next Steps

Quick Answer

The main alternatives to a reverse mortgage in Canada are a HELOC, a conventional refinance, downsizing, drawing from registered accounts, a no-payment term mortgage for under 55 or high-value properties, and provincial property tax deferral programs. The reverse mortgage is typically the best fit when income qualification is not available, the borrower intends to stay in their home, and the no-payment structure is the primary need.

Summary Table

| Alternative | Monthly Payment | Income Required | Age Limit | Stays Home | Recourse |

|---|---|---|---|---|---|

| Reverse Mortgage | None | No | 55+ | Yes | No — guaranteed |

| HELOC | Interest required | Yes | None | Yes | Full recourse |

| Conventional Refinance | Required | Yes | None | Yes | Full recourse |

| Second Mortgage | Required | Yes | None | Yes | Full recourse |

| Downsizing | N/A | N/A | None | No | N/A |

| Rental Income | N/A | N/A | None | Yes (partial) | N/A |

| Registered Account Draws | N/A | N/A | N/A | Yes | N/A |

| No-Payment Term Mortgage | None during term | Partial | None | Yes | Full recourse |

| Property Tax Deferral | None | Varies | 55+ typical | Yes | Charge on title |

HELOC

Lower rate, more flexible — but requires income qualification, monthly interest payments, and is callable. The lender can freeze or reduce it at any time, for any reason, without notice.

Best for homeowners who can qualify on income, have the cash flow to service the monthly payment reliably, and have a short-term or revolving need. Not available to most retirees on fixed incomes at a meaningful amount.

Good fit for: Homeowners with reliable income, can qualify, have a short-term or revolving need

Poor fit for: Retirees on fixed CPP/OAS who may not qualify at a meaningful amount, or who need a stable facility that cannot be frozen

For the complete reverse mortgage vs. HELOC comparison — including the HELOC income trap — see Reverse Mortgage vs. HELOC Canada.

Conventional Mortgage Refinance

Refinancing at a conventional mortgage rate — lower than a reverse mortgage — with mandatory monthly payments and income qualification required. Up to 80% of appraised home value. Best for homeowners with qualifying income who want the lowest rate. Not available to most retirees on fixed incomes at a meaningful amount.

Good fit for: Homeowners with qualifying income who want the lowest possible rate and can manage increased monthly obligations

Poor fit for: Retirees with modest income who cannot qualify; anyone for whom a mandatory payment is the problem being solved

For how the reverse mortgage compares on monthly payment obligations — see Reverse Mortgage vs. HELOC Canada.

Second Mortgage

A loan secured behind the first mortgage. Higher rate than a first mortgage. Requires income qualification and monthly payments. Best for short-term bridge financing where preserving the first mortgage rate is important.

Good fit for: Short-term bridge financing or a specific large one-time expense where preserving the first mortgage is important

Poor fit for: Long-term income supplementation or situations where monthly payments are already a constraint

The Canada Reverse Mortgage Guide — Yours, Free

"I wrote this guide the same way I'd explain it to a friend over coffee — no jargon, no sales pitch, just the straight goods on how reverse mortgages work, who they're right for, and what to watch out for."

📥 Download Your Free Guide

Instant download — no credit card, no spam, no obligation.

🔒 Your info stays private. Unsubscribe anytime. Zero spam. Promise.

Downsizing

Selling the current home and buying a smaller, less expensive one releases the equity difference as cash. But downsizing has a hidden cost most people significantly underestimate.

| Cost Item | Applies to | Typical Range |

|---|---|---|

| Real estate commissions (~5% of sale price on a $900K home) | Sale | ~$45,000 |

| GST/HST on commission (5% to 15% depending on province) | Sale | ~$2,250–$6,750 |

| Legal fees — sale | Sale | $1,500–$3,000 |

| Legal fees — purchase | Purchase | $1,500–$3,000 |

| Land transfer tax — provincial (purchase only · AB/SK lowest, BC/ON/QC highest) | Purchase only | ~$650–$10,000+ |

| Municipal land transfer tax — Toronto only (effectively doubles the provincial) | Purchase only | ~$8,000–$10,000 additional |

| Moving, storage, and transition costs | Sale | $5,000–$15,000 |

| Potential renovation of new property | Purchase | Variable |

| Total transaction costs | $60,000–$100,000+ in major markets |

The net equity released is often significantly less than it appears. Selling a $900,000 home and buying a $600,000 condo releases $300,000 in theory — but real transaction costs typically consume $60,000 to $80,000 of that gap.

A hybrid worth considering: sell the larger home, use a reverse mortgage to fund part of the purchase on the smaller home, and keep the balance as liquid savings. Critical rule: the lender must confirm acceptance of the new property before any purchase contract is signed. Never waive a financing condition on a reverse mortgage purchase.

Good fit for: Homeowners who genuinely want to move and have run the actual net numbers after transaction costs

Poor fit for: Someone considering it only to access equity — the transaction costs make it a sensible financial move only for those who actually want to move

For when the timing of a home equity decision matters — see Post 14: Why Waiting Could Cost You More.

Renting Out a Portion of the Home

A basement suite or secondary dwelling generates income from an existing asset without selling or borrowing. Rental income is taxable. Renting part of the principal residence may have implications for the principal residence exemption at eventual sale. A tax advisor should be consulted before proceeding.

Good fit for: Homeowners with suitable properties in rental-demand markets who are comfortable with the responsibilities

Poor fit for: Those who prefer full privacy or cannot manage the physical or administrative demands

The Renovation-to-Rental Strategy

One of the more underappreciated uses of a reverse mortgage is as renovation capital — specifically to create a rental suite where one does not yet exist.

The logic is straightforward. A homeowner draws from the reverse mortgage to fund the renovation. A finished suite adds rental income. That income can be used — in full or in part — to make voluntary interest payments on the reverse mortgage each month, keeping the running balance lower than it would otherwise be. Meanwhile, the finished suite adds to the appraised value of the property, which can also increase the available equity for future draws.

Three things happen simultaneously:

1. Income is created. A basement suite in a major Canadian market can generate $1,500 to $2,500 per month in rental income. Even applying half of that to monthly interest on a $150,000 renovation draw at 7% keeps the balance from compounding at the full rate.

2. Home value increases. A legal secondary suite adds measurable appraised value — often more than the cost of the renovation in strong rental markets. This expands the equity cushion and improves the estate position over time.

Balance growth slows. Canadian reverse mortgage lenders allow voluntary payments. A borrower making even partial monthly interest payments changes the long-term balance trajectory substantially. The obligation is gone — the option remains — and rental income provides a natural funding source for it.

This strategy works best for homeowners whose property has suite potential, who are comfortable being landlords (or can manage it through a property manager), and who want to use home equity productively rather than passively. It converts a dormant asset — the unfinished basement — into an income-generating one, using equity that was already locked in the home.

A broker prequalification can model the renovation draw, the projected rental income, and the net balance trajectory with and without voluntary payments — so the numbers are concrete before any decision is made.

Note: rental income is taxable and renting part of a principal residence may have implications for the principal residence exemption at eventual sale. Always consult a tax advisor before proceeding.

Good fit for: Homeowners with suite-ready properties, in rental-demand markets, who want to convert equity into income and manage balance growth actively

Poor fit for: Those who prefer full privacy, properties unsuitable for secondary suites, or homeowners unwilling to take on landlord responsibilities

Drawing From Registered Accounts

RRIF and RRSP withdrawals are fully taxable as income. Large withdrawals push taxable income higher — potentially triggering the OAS clawback, increasing the tax bracket, and reducing GIS eligibility.

TFSA withdrawals are tax-free with no income impact — the most efficient registered draw, but limited by account balance and annual room.

Using a reverse mortgage to reduce RRIF withdrawals keeps taxable income lower, preserves registered assets for longer, and extends the runway of the retirement income plan. A reverse mortgage draw is not income and has no tax consequences — compared to RRIF withdrawals (fully taxable), investment liquidations (capital gains), or RRSP draws (fully taxable), a reverse mortgage is typically the most tax-efficient supplemental income source for homeowners with significant equity.

Here is how the comparison plays out in practice. A retiree with $400,000 in an RRIF, $650,000 in home equity, and $28,000/year in CPP and OAS has two ways to generate an additional $24,000/year in spending money:

RRIF withdrawal route: Add $24,000 in RRIF withdrawals. Pushes total taxable income to $52,000. At Ontario marginal rates, roughly $7,000 goes to tax. Net after-tax income from the withdrawal: approximately $17,000. The RRIF depletes faster and the OAS clawback threshold (approximately $90,000) is not yet a concern — but the tax drag compounds year over year as the RRIF balance shrinks and future mandatory minimums grow as a percentage.

Reverse mortgage draw route: Draw $24,000 from home equity. Tax return unchanged. OAS and GIS unaffected. RRIF continues to compound tax-sheltered. The interest building on the reverse mortgage balance is real — but the after-tax cost of a 6.5% reverse mortgage draw is often lower than the effective tax cost of an equivalent RRIF withdrawal when you include the bracket impact.

The optimal strategy for most retirees is a combination: TFSA first (tax-free), then a blend of RRIF (taxable) and reverse mortgage draws sized to keep total taxable income below thresholds that would trigger the OAS clawback or push into a higher bracket.

For a full model of how reverse mortgage draws interact with RRIF drawdown, CPP deferral, and OAS clawback protection — see The Complete Retirement Financial Plan.

The HELOC Qualification Gap Most People Don't Anticipate

Many Canadians assume they'll qualify for a HELOC and a reverse mortgage when they need income. In practice, the HELOC option is often not available at a useful amount.

A stress-tested HELOC qualification in retirement: the lender applies a stress test at the higher of the current rate plus 2% or a regulatory minimum. For a retiree with $28,000/year in CPP and OAS income, the total debt service capacity is limited. On $2,333/month gross income, a conventional HELOC lender applying a 30% GDS ceiling would permit roughly $700/month in total housing costs — including property taxes, insurance, and HELOC interest. After property taxes and insurance, there may be very little left for HELOC interest service.

The result: a retiree with $700,000 in home equity may be offered a $40,000 to $60,000 HELOC — not the $200,000 to $250,000 they were expecting. The reverse mortgage for the same borrower might approve $280,000 to $315,000. The gap isn't a rounding error.

This is why the HELOC vs. reverse mortgage comparison is often theoretical. The reverse mortgage isn't chosen over the HELOC — it's chosen because the HELOC isn't actually available at a useful amount.

No-Payment Term Mortgage

Available on freehold properties in Ontario, Alberta, and BC for homeowners of any age. Up to 60% LTV on a 1-year term, no monthly payment during the term.

| Term | Maximum LTV | Minimum Credit Score |

|---|---|---|

| 1 year | 60% | 550 |

| 3 years | 49.5% | 660 |

| 4 years | 46% | 660 |

| 5 years | 43% | 660 |

The structural differences from a reverse mortgage are significant: no negative equity guarantee (full recourse loan), renewal not guaranteed, full balance due at term end, solid exit plan required before signing, broker fee may apply (always disclosed in writing), minimum loan $100,000.

Good fit for: Under-55 homeowners or 55+ with high-value properties; borrowers with a specific time-limited need and a credible exit plan

For a complete side-by-side comparison of the two products — see Post 26: Term Mortgage vs. Reverse Mortgage.

Property Tax Deferral Programs

Several provinces offer deferral programs that allow senior homeowners to defer some or all of their annual property taxes through a government-backed low-interest loan, repaid when the home is eventually sold. This addresses the reverse mortgage's most common default trigger — unpaid property taxes — and in most provinces can be used alongside a reverse mortgage.

| Province | Program | Link |

|---|---|---|

| BC | Provincial program — 55+. Note: from 2026, compound interest at Prime + 2% on deferred amounts | gov.bc.ca |

| Alberta | Provincial program — 65+, minimum 25% home equity | alberta.ca |

| Saskatchewan | Education portion of taxes only — qualifying seniors | saskatchewan.ca |

| Manitoba | Provincial program under Seniors' Property Tax Deferment Act — contact municipality | gov.mb.ca |

| Ontario | No broad provincial program — municipal programs vary. Contact your local municipality | ontario.ca |

| New Brunswick | Provincial program — defers annual increase in taxes on principal residence | gnb.ca |

| Nova Scotia | Rebate (not deferral) — 50% of municipal taxes up to $800 for GIS recipients | novascotia.ca |

| PEI | Program available — contact Service PEI for eligibility | princeedwardisland.ca |

| QC, NL & territories | No broad provincial program — contact your local municipality | — |

Enrolling in a deferral program also satisfies the reverse mortgage condition to keep property taxes current — eliminating one of the most common default triggers. In most provinces, property tax deferral can be used whether or not a reverse mortgage is in place.

For the full eligibility breakdown including property tax obligations — see Reverse Mortgage Eligibility Canada.

How to Choose

The right alternative depends on honest answers to a few questions:

Do you want to stay in your home, or are you open to moving?

Can you reliably service monthly payments from your retirement income?

Can you qualify for conventional financing based on income?

Is leaving maximum estate equity an important goal?

Do you need a facility that cannot be frozen or reduced?

Is tax efficiency of the draw method important to your income plan?

Running the actual numbers for each option — with your specific home value, age, income, and timeline — makes the comparison real.

See what a reverse mortgage would provide in your specific situation — try the free calculator.

Frequently Asked Questions

Is a reverse mortgage better than downsizing?

It depends on whether you actually want to move. Downsizing releases more equity in theory — but after real estate commissions, HST on those commissions, legal fees on both transactions, land transfer tax on the purchase of the replacement property, and moving costs, the net equity released is often $60,000 to $80,000 less than the gross gap. For homeowners who want to stay, the reverse mortgage is almost always the better tool.

What is the most tax-efficient way to access home equity in retirement?

A reverse mortgage draw is not income and has no tax consequences. Compared to RRIF withdrawals (fully taxable), investment liquidations (capital gains), or RRSP draws (fully taxable), a reverse mortgage is typically the most tax-efficient supplemental income source for homeowners with significant equity.

Can I use property tax deferral alongside a reverse mortgage?

Yes — in most provinces, property tax deferral is available regardless of whether a reverse mortgage is in place. Enrolling eliminates one of the most common default triggers entirely. Confirm the specific provincial program terms.

Is a reverse mortgage always the most expensive option?

In nominal rate terms, a HELOC typically carries a lower rate. In total cost of ownership — transaction costs, mandatory payment obligations, callability risk, tax implications, and long-term rate-at-reset differences — the comparison is more nuanced than the rate alone suggests.

Next Steps

See what a reverse mortgage would provide in your situation:

Get a full comparison of all options modelled to your situation:

Keep reading:

Reverse Mortgage Canada — The Complete Guide · Post 5: The Complete Retirement Financial Plan

Reverse Mortgage vs. HELOC Canada · Post 9: 5 Ways to Eliminate Debt in Retirement

Reverse Mortgage Eligibility Canada · Post 25: Under 55 and Need Home Equity?

Reverse Mortgage FAQ Canada · Post 19: Is a Reverse Mortgage Right for You?

- keep Learning -

Straight Talk from the Blog

Plain-language articles to help you make better decisions. No fluff, no filler — just what you actually need to know.

Grey Divorce in Canada After 60: Housing and Equity Options You Should Know

Divorcing after 60? Learn how to navigate grey divorce in Canada with smart housing strategies and home equity solutions that don’t require income or traditional financing. ...more

Protected HELOC Basics ,Women & Finance &Divorce & Money

October 12, 2025•4 min read

How Retirees in Canada Can Use Home Equity Without Losing Control

Explore smart ways for Canadians 60+ to unlock their home equity without risking financial flexibility. Learn how the Protected HELOC® offers secure, customizable access to retirement cash flow. ...more

Retirement Planning ,HELOC vs Reverse Mortgage Reverse Mortgage Alternatives &Retirement Income Strategies

October 09, 2025•3 min read

Where Does Canada's Reverse Mortgage Industry Go From Here? What New Lenders Mean for Borrowers

Canada's reverse mortgage market has more lenders than ever. Here's what that competition means for rates, products, and borrower outcomes — and what to watch going forward. ...more

Deeper Canadian Context

April 24, 2026•8 min read

The Reverse Mortgage and the Estate Plan — 4 Things Every Canadian Family Should Discuss

A reverse mortgage affects the estate. Here are the 4 conversations every Canadian family should have before — and after — one is signed. ...more

Family & Advisors

April 15, 2026•8 min read

What Your Estate Lawyer Needs to Know Before Your Client Signs a Reverse Mortgage

Estate lawyers in Canada are increasingly encountering reverse mortgages in client files. Here's the plain-English briefing on how they work, what to watch for, and where the legal touchpoints are. ...more

Family & Advisors

April 06, 2026•8 min read

Why Most Financial Advisors Get Reverse Mortgages Wrong — and What a Good One Does Instead

Most Canadian financial advisors default to "avoid it" on reverse mortgages. Here's what the evidence actually says — and what a genuinely client-focused advisor does with it. ...more

Family & Advisors

March 31, 2026•8 min read

How Do You Split a House Without Selling It? The Equity Buyout Most Divorcing Couples Never Consider

When one spouse wants to keep the house in a grey divorce, a reverse mortgage can fund the buyout — no sale, no income qualification, no forced timeline. Here's how it works. ...more

Making Your Decision

March 21, 2026•11 min read

Grey Divorce — You Kept the House. Now What?

You kept the house in the divorce. Now you can't qualify for a new mortgage on your own, and the equity is locked. Here's what Canadian homeowners 55+ can do. ...more

Making Your Decision

March 20, 2026•12 min read

Your Retirement. Your Equity. Your Options

Let's build a plan that gives you confidence for today and freedom for tomorrow.

- Your Trusted Advisors -

- Explore Our Resources -

Canada's trusted plain-language resource for reverse mortgage information. Helping Canadian homeowners 55+ unlock the value in their homes with confidence, clarity and a plan for a better retirement.

Two experienced professionals. One common goal: Helping you make informed decisions with confidence.

Matthew Hines CRMS, CSEC

Mortgage Agent Level 2

Matthew has spent two decades helping Ontario homeowners navigate the decisions that matter most in retirement. He holds the Canadian Reverse Mortgage Specialist (CRMS) designation, works with Canadian reverse mortgage lenders, and co-authored the Canada Reverse Mortgage Guide. His approach is simple: understand the whole picture first, then find the structure that actually fits — even if that structure isn't a reverse mortgage.

647-372-0762 | Mon – Fri: 9am – 6pm EST

Gregory Stanley CFP, CSEC

Mortgage Broker

Gregory has spent decades helping homeowners across BC and Alberta build retirement plans that actually hold up under pressure. As a Chartered Financial Planner and co-author of the Canada Reverse Mortgage Guide, he brings a planning lens most mortgage brokers don't have — which means the reverse mortgage conversation always happens inside the bigger picture, not instead of it.

236-300-3439 | Mon – Fri: 9am – 6pm PT

Independent Advice

We are not owned by any lender. Your best interests come first.

Education First

Clear information so you can make confident decisions

Private & Secure

Your information is never shared. Your privacy is always protected.

100% Canadian

We understand Canadian Home Owners, because we are one.

Copyright 2026. Stanley-Hines. All Rights Reserved. Privacy Policy | Sitemap

Reverse mortgage loans are provided by Canadian lenders. Terms, conditions and rates apply. This site is for educational purposes only and does not constitute financial or legal advice. Please speak with a qualified professional to discuss your specific situation.

%20(1)%20(1).jpg)