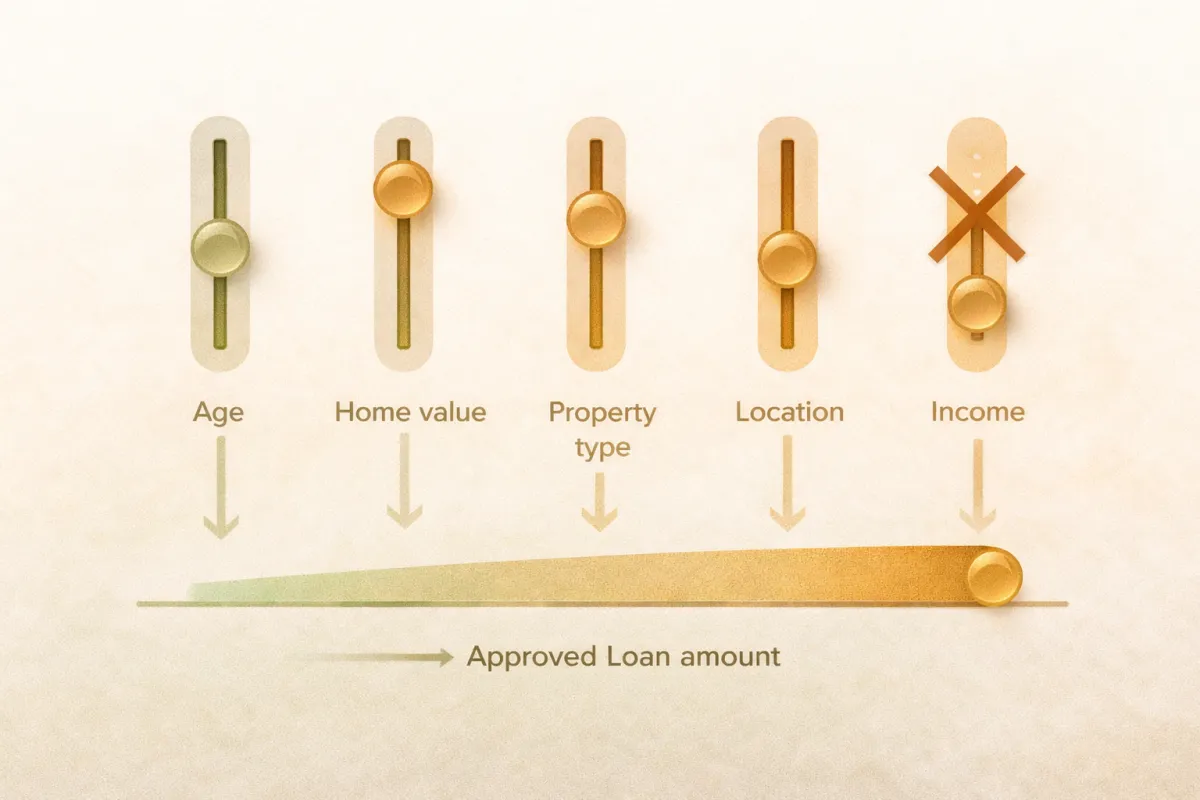

4 Things That Determine How Much You Can Borrow — and 1 Thing That Doesn't

Most Canadians who research reverse mortgages for the first time ask the same question early in the process: how much can I actually get?

It is the right question. And the answer involves four specific factors — and one notable absence that surprises almost everyone.

The factor that does not determine how much you can borrow in a reverse mortgage is income.

Unlike a conventional mortgage, a HELOC, or a personal loan, a reverse mortgage does not require income qualification. The lender does not ask for pay stubs, T4s, tax returns, or confirmation of employment. Your CPP, OAS, pension, investment income, or employment status has no bearing on the approved amount.

This is the feature that makes the reverse mortgage uniquely accessible to retirees on fixed incomes — and the feature that surprises most people who have spent their lives qualifying for credit based on what they earn.

Here are the four things that actually determine the amount.

Factor 1 — Age

Age is the most important factor in a reverse mortgage approval. The older the borrower, the higher the percentage of the home's value that can be borrowed.

The logic is actuarial. A 55-year-old borrower is statistically likely to hold the mortgage for a longer period than a 75-year-old. The longer the mortgage is in place, the more the balance grows — and the more the lender depends on the property's value at repayment covering the outstanding balance. To manage this risk, younger borrowers receive a lower percentage of the home's value.

As a rough guide — and these figures vary by lender, property type, and location:

At 55, the approved amount is typically in the range of 20–30% of the home's value

At 65, the approved amount is typically in the range of 30–40%

At 75, the approved amount is typically in the range of 40–50%

At 80+, the approved amount can approach or slightly exceed 50% depending on the lender

These are illustrative ranges, not guarantees. The specific figure for any individual situation requires a proper assessment. Use the Canada Reverse Mortgage Calculator for a personalised estimate.

For couples, the approved amount is calculated based on the age of the younger borrower — the person who is statistically likely to hold the mortgage longest. This is worth understanding when deciding whether to include a younger spouse on the application. Including a younger spouse means the approved amount is based on their age rather than the older partner's. Excluding them means the mortgage becomes due on the first death, rather than continuing until the last borrower passes away. Both have tradeoffs worth discussing with a broker.

Factor 2 — Home Value

The home's appraised value is the second major factor. The approved loan amount is a percentage of what the property is worth — the higher the value, the higher the potential loan amount in dollar terms.

The lender orders an independent appraisal of the property. This is not the municipal assessment, the Zestimate, or what a neighbour sold for — it is a formal appraisal conducted by a qualified appraiser. The appraisal determines the value the lender uses to calculate the maximum loan amount.

For a property worth $600,000 at a 35% approval rate, the maximum loan amount is $210,000. For a property worth $1,200,000 at the same 35% approval rate, the maximum is $420,000.

The relationship is linear — higher home value, higher dollar amount available — which is why reverse mortgages are often most impactful in markets where property values are substantial. In Toronto, Vancouver, and other high-value markets, the dollar amounts available through a reverse mortgage can be significantly larger than in lower-value markets, even at the same percentage.

Factor 3 — Property Type

Not all properties qualify, and not all qualifying properties are treated equally.

The standard qualifying property for a reverse mortgage in Canada is a single-family detached home — the most straightforward case. For other property types, lenders apply their own assessments.

Condominiums: Generally eligible, but subject to lender-specific conditions. The condo corporation's financial health, the building's age, and the unit's location within the building can all affect eligibility. Some lenders are more conservative on condominiums than others.

Semi-detached and townhouses: Generally eligible, though lenders assess these on the same basis as detached homes — condition, marketability, location.

Rural properties: Subject to more conservative assessment in many cases, particularly if the property is on well and septic rather than municipal services, or if the rural location affects marketability. Some rural properties may not qualify or may qualify at a reduced percentage.

Cottages and seasonal properties: Not eligible. A reverse mortgage is available only on the primary residence — the home the borrower actually lives in.

Properties with significant deferred maintenance: A lender will decline or reduce the approved amount for a property that is not in good condition. This is both a qualification issue and an ongoing condition of the mortgage — the property must be maintained throughout the life of the mortgage.

Property type assessment is one of the reasons a broker who knows all four lenders is valuable. Different lenders have different thresholds for different property types. A property that one lender declines may qualify with another.

Factor 4 — Location

Location affects the approved amount through two mechanisms: the property's marketability and the lender's geographic risk assessment.

Marketability is the lender's assessment of how easily the property could be sold to recover the outstanding balance if necessary. A property in a major urban centre with high transaction volume and stable demand is more marketable than one in a small town with limited buyer activity. Higher marketability supports a higher approval percentage.

Lender geographic coverage also matters. Not all lenders operate in all parts of Canada with equal confidence. A property in a well-served urban market may receive a more generous assessment than one in a remote or low-density area. Some lenders have explicit geographic restrictions — properties must be within a certain distance of a major centre, or in certain provinces.

This is another reason the four-lender comparison matters. A property in a location where one lender is conservative may be assessed more favourably by another.

The Factor That Doesn't Matter — Income

To return to the beginning: income does not determine how much you can borrow in a reverse mortgage.

This deserves emphasis because it runs counter to every other lending experience most Canadians have had. A mortgage application, a car loan, a HELOC, a credit card increase — all of these involve income verification. The lender wants to know that the borrower can service the debt.

A reverse mortgage has no debt service requirement. There are no mandatory monthly payments. The balance grows over time and is repaid when the home is sold. The lender's security is the property itself — not the borrower's income.

This means a retiree with $2,000 per month in CPP and OAS income and a $900,000 home qualifies for the same percentage of the home's value as someone with a $200,000 annual salary and the same home. Income is simply not in the calculation.

There are a small number of income-adjacent considerations — the lender confirms the borrower can maintain the basic ongoing obligations of the mortgage, including property taxes and home insurance. But this is not income qualification in the conventional sense. It is a capacity assessment, and it is a much lower bar than conventional mortgage qualification.

The Practical Implications

Understanding what determines the approved amount has several practical implications for anyone considering a reverse mortgage:

Age determines the percentage — waiting increases it. For a borrower who is 62 and considering a reverse mortgage, waiting three years to 65 increases the approved percentage and the dollar amount available. Whether the benefit of waiting exceeds the cost of the delay — in unaddressed financial need, in debt continuing to accumulate — is a calculation worth doing explicitly.

Home value is the multiplier. Investments in the home that increase its appraised value also increase the available reverse mortgage amount. A well-maintained, well-presented home at appraisal maximises the available loan.

Property type and condition affect both eligibility and amount. A broker who assesses the property before the application — and who knows which lenders are most favourable for specific property types — saves time and produces better outcomes.

Income is irrelevant to the approved amount — but relevant to the plan. While income does not determine how much can be borrowed, it does inform how much should be borrowed. The right draw amount is the one that addresses the genuine financial need without drawing more than necessary. A complete retirement income plan — including CPP, OAS, registered account drawdowns, and reverse mortgage draws — produces a better outcome than treating the reverse mortgage as an isolated decision.

The Plain-English Summary

Four things determine how much you can borrow in a Canadian reverse mortgage: your age, your home's appraised value, your property type, and your location.

One thing that does not: your income.

The specific amount available for any individual situation is best estimated through the calculator at canadareversemortgageguide.ca/reverse-mortgage-calculator and confirmed through a broker assessment across all four lenders.

[Get Your Free Comparison at Canada Reverse Mortgage Guide →]

This article is for educational purposes only and does not constitute financial, tax, investment, or mortgage advice. Approved amounts, LTV ratios, and lender requirements vary and change over time. All percentage ranges are illustrative only. A licensed Canadian mortgage broker can provide a personalised assessment for your specific situation. All reverse mortgage products are subject to individual lender approval and terms.